发布时间: 2022/01/14 关注度: 1191

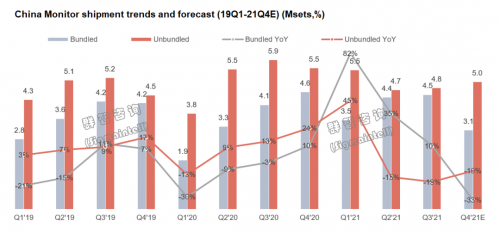

In 2021, the Chinese monitor market will still deliver a relatively satisfactory answer after going through various tests. According to Sigmaintell data, China's monitor shipments will reach 35.42 million units in 2021, an increase of about 2.5% YoY. In 2022, China's monitor shipments will remain at a high level of about 35.11 million units, down about 1% YoY.

In terms of bundling monitors, considering that the last orders of the Xinchuang project have been completed one after another, and the new eight major industries need to change machines, the driving force for pulling goods is not as strong as that of the Xinchuang project. Sigmaintell predicts that the size of China's bundling monitor market will decline by about 4.5% in 2022. In terms of independent monitors, the shortage of graphics cards will continue in the first half of next year, and the shipment of gaming monitors will face greater resistance in the first half of the year, and it is expected to improve in the second half of the year. Secondly, it is difficult to return to the low-cost era, which has an impact on brand mentality and shipping momentum. Under the combined influence, Sigmaintell expects that the size of China's independent monitor market will grow by about 2% in 2022.

Brand pattern: The territory is rewritten, and the market is brewing new changes.

In 2021, China's independent monitor market shows a trend of upward commercial use and downward consumption. The brand layout has been reshaped, and the dominance of top brands has changed. Mid-segment brands and new entrants have gained a share, while local brands have lost their share. In 2022, the overall pattern of independent monitor brands in China will still be in a period of continuous dynamic adjustment. The core of this is the shrinking of the scale of leading brands. The release of the market share provides more market space for mid-range brands and new entrants.

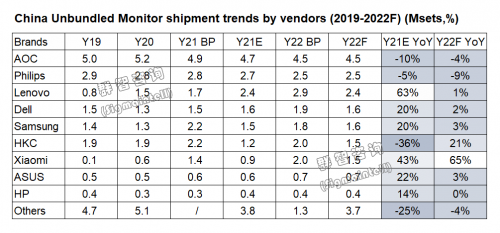

AOC: Although it is generally limited by the tight supply of graphics cards, thanks to its supply chain advantages, its gaming monitors showed slight growth. The market share of its curved gaming monitors has shrunk significantly, the market share of high-resolution monitors has shrunk, the market share of professional color monitors has been stable, and portable monitors have grown rapidly. In 2021, the shipment scale is 4.68 million units, a decrease of 10% YoY. There is a 4% gap between the actual shipment scale and the planned target. About 4.5 million units are planned to be shipped in 2022, which is a conservative plan. In 2022, the overall strategy will change from the pursuit of scale growth to the pursuit of profit growth.

Philips: In 2021, its size structure is more influenced by supply. Among the major consumer product lines, the supply of small-sized products under 23 inches is tight, especially the rapid decline in 21.5-inch shipments. The entry-level commercial series lacked price competitiveness due to cost issues, and its share began to decline in the second quarter, and it lacked growth momentum in the second half of the year. In 2021, the shipment scale will be 2.7 million units, a decrease of 5% YoY. There is a 4% gap between the actual shipment scale and the planned target. In 2022, about 2.5 million units are planned to be shipped, and the contraction rate is larger than that of AOC. In 2022, Philips will show a certain differentiation from AOC in terms of market layout. The former will make clearer product line adjustments in the commercial market while reducing the focus of shipments in the offline consumer market. Philips' shipment target for the online market next year remains relatively aggressive.

Lenovo: Lenovo has achieved impressive growth in the discrete monitor market in 2021, mainly relying on its multi-brand strategy. ThinkVision focuses on the commercial market. Lecoo, as a rapid march in the consumer market, has enhanced the influence of the DIY market, and its new brand-ability has entered the monitor market. In 2021, Lenovo's independent monitor shipments will be about 2.47 million units, an increase of 63% YoY. Thanks to the Xinchuang project, the B2B growth rate reach 73% in 2021; the B2C growth rate is 53%. The growth is mainly attributable to the DIY market, where both Lenovo and its sub-brand Lecoo perform well. About 2.85 million units are planned to be shipped in 2022. Next year, the B2B growth rate will shrink, and the growth will mainly come from the consumer market.

Dell: Poor stocking in the first half of 2021 affects shipment performance, which in turn restricts its performance in the main professional color monitor market, and the proportion of large products such as 27 inches shrank. To alleviate the supply problem of general-purpose models, Dell imported panel makers from the mainland. The supply situation of 19.5 and 23.8 inches in the third quarter improve slightly. With the improvement of the overall supply situation in the second half of the year, the scale of shipments has recovered. In 2021, the shipment scale is 1.56 million units, an increase of 20% YoY. In 2022, it plans to ship about 1.9 million units, pursuing growth of about 22% YoY.

Samsung: In 2021, under the influence of the epidemic, Samsung's Vietnam factory is difficult to produce, and the overall supply situation has deteriorated. At the same time, the price of 23.8-inch products remains high, which significantly inhibits demand, but its price strategy for 27-inch products, which is the main force in the consumer market, is relatively positive. The high proportion of curved gaming monitors has affected its gaming monitor shipments to a certain extent. In 2021, Samsung ship about 1.51 million units, an increase of 20% YoY. About 1.8 million units are planned to be shipped in 2022. Its overall strategy next year will be to actively seek product structure upgrades.

Gaming market: Entering a growth bottleneck due to supply issues. 240Hz is coming to the fore.

The shipments of China's gaming monitor market in the second half of 2021 did not meet expectations. The main reasons include: on the one hand, the repeated local epidemics caused many Internet cafes to close again, and the demand for Internet cafes is still relatively sluggish; on the other hand, because the supply of graphics cards hasn't been significantly improved, whether it is online or Internet cafes, the demand for gaming has been suppressed or shifted.

According to Sigmaintell data, China's gaming monitor shipments is about 3.6 million units in 2021, an increase of only 1% YoY. As can be seen from the historical data of the same period, this year is the lowest growth rate since the beginning of the Chinese gaming market. In 2022, combined with the graphics card supply time rhythm, brand shipping mentality, and the strict trend of local epidemic prevention and control, the overall lack of strong growth momentum. Therefore, the shipment scale in 2022 is expected to be about 4.2 million units, a slight increase of 16% YoY.

Although the market size increment is limited, the Chinese gaming market in 2021 will show positive changes in structural upgrading, mainly manifested in the emergence of 240Hz. In 2021, the 240Hz shipment in the Chinese gaming market is about 180,000 units, and the penetration rate in the gaming market is close to 5%. Driven by the product strategies of leading brands TPV and professional gaming brands such as ASUS, the 240Hz shipment scale is expected to be around 380,000 units in 2022, with a penetration rate of close to 9%, ushering in the first year of development.

Curved market: The trough period is coming, and supply chain adjustment and cost increase are the main reasons.

In 2021, the shipment scale of China's curved monitor market is about 2.4 million units, a decline of 36% YoY. The main reason is that the overall supply of curved products has not improved significantly, and the end price is still at a high level. As far as the current monitoring of the average price of the end is concerned, except for the curved market, the average price of each market segment has begun to fall, but the price increase of the curved products has further expanded. Coupled with the impact of gaming graphics cards on gaming monitors, the proportion of curved gaming has further declined, resulting in a rapid shrinking of the curved market.

Overall, it can be seen that the current tight supply of curved monitors and graphics cards harms curved gaming, causing the curved market to enter a "trough period". After these two negative factors ease, it is expected to usher in a rebound in the curved monitor market.

Ultrawide market: Slow growth, supply improvement, and diversification in the following year will unlock new opportunities.

In 2021, China's ultrawide monitor market shows a recovery trend in the second half of the year. Its momentum is mainly due to changes in the brand structure, and the market growth is driven by the newly entered brand Huawei.

In 2021, ultrawide shipments are exceeded 550,000 units, an increase of about 7% YoY. Combined with the exponential growth and diversified development trend of ultrawide panels in 2022, Sigmaintell predicts that China's widescreen market will grow by about 19% YoY.

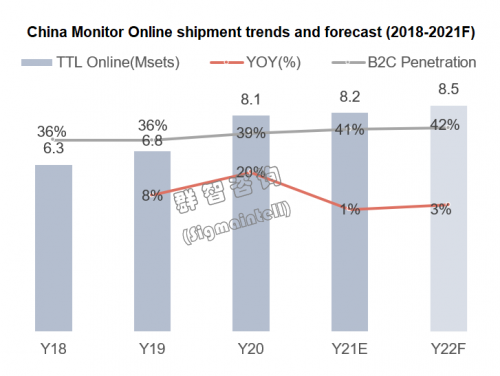

Online market: The growth is limited, but the advantage of the center of gravity is prominent, and it is expected to remain in the next year.

After the epidemic, a new life form of online work and study has been formed, and the monitor has become a rigid demand, which has accelerated the development of online consumption habits. In China's independent monitor market, the share of the online market has increased quarter by quarter. In the first half of 2021, the sales volume of China's independent monitor online market is close to 400 units, and the sales volume in the second half of the year is expected to be about 4.1 million units.

In the online market, AOC accounts for about 30%, and online channels are generally weak, and negative growth will continue from 2021 to 2022. Affected by price fluctuations and its emphasis, Philips' online channel accounts for only about 20%, but it will strengthen its online channel capabilities next year. Dell and Samsung's online channels accounted for a balanced proportion, remaining at around 50%.

According to data from Sigmaintell, the sales volume of China's online monitor market in 2021 is about 8.2 million units, a slight increase of 1% YoY. In 2022, affected by the brand's overall focus on online and the channel's focus on commercial development strategies, it is expected that China's online monitor market will continue to grow and exceed 8.5 million units.

Sigmaintell suggests: In the post-epidemic era, market risks and opportunities are magnified together.

Entering the post-epidemic era, in 2022, the risks and opportunities of China's monitor market will still be magnified together. Risks: At the macro level, China's domestic demand economy will continue to be under pressure; at the middle level, the unemployment rate of the main population in the monitor consumer market will continue to increase; at the micro-level, people's consumption expenditure will turn conservative. The superposition of various factors will significantly magnify the demand risk in China's monitor market in 2022.

However, from the perspective of opportunities, there are still good opportunities for market development. Firstly, the supply situation has improved significantly. With the gradual fading of the global consumer electronics epidemic dividend, the supply of monitor panels will improve significantly; secondly, the cost situation will change. Affected by the improvement in supply, the cost of monitor panels will also be adjusted, and panel prices will be dehydrated, which is beneficial to the end. Stability and fall in selling prices; thirdly, fierce competition in monitor supply will help promote high-end technology sinking and market structure upgrade, especially in high-end technologies such as 240Hz, ultrawide, MiniLed, and OLED. In summary, Sigmaintell makes the following recommendations:

1. Well-organized product line. The product line should be sorted out and planned according to the target customers and its brand characteristics, to achieve comprehensive coverage of customers, and at the same time accurately reflect the brand positioning. According to the different attributes of the consumer market and the commercial market, flexible and targeted product upgrades are carried out in terms of size, resolution, frequency rate, and flat and curved structure to enhance market competitiveness.

2. Catch the trend of gaming monitors. At present, the development of market segments other than gaming monitors is relatively slow, so it is the top priority to focus on mining the gaming monitor market. The product line is divided into ordinary players and gaming players. The former pays attention to the comprehensive performance of the screen and emphasizes cost performance. The latter is more subdivided, and a professional product line layout is carried out according to the game attributes of players, emphasizing professionalism, and aiming at a high-frequency rate, ultra-high frequency rate, and high resolution for selective enhancement.

中文:

着眼于2021年全年,中国显示器市场经历种种考验后,依然交出了相对令人满意的答卷。群智咨询(Sigmaintell)数据显示,2021年中国显示器出货规模达到3542万台,同比增长约2.5%;展望2022年,中国显示器出货规模将保持在3511万台左右的高位,同比下滑1%左右。

在捆绑显示器方面,考虑到信创项目尾单陆续完成,而新开出的八大行业换机需求,拉货动力没有信创项目强劲,群智咨询(Sigmaintell)预计2022年中国捆绑显示器市场规模将下滑4.5%左右。在独立显示器方面,显卡明年上半年缺货情况会持续,电竞显示器上半年出货阻力较大,好转有望在下半年发生。其次,低成本时代难以回归,对品牌心态和出货动力有所影响。综合影响下,群智咨询(Sigmaintell)预计2022年中国独立显示器市场规模将增长2%左右。

品牌格局:版图改写,市场酝酿新变局

2021年中国独立显示器市场整体呈现商用向上、消费向下的走势,品牌格局表现为市场版图重塑,头部品牌独大的情况发生改变,中段品牌和新入局品牌取得份额增长,本土品牌份额失守。2022年中国独立显示器品牌格局整体仍处于持续性的动态调整期,调整核心来自于头部品牌规模收缩,市场份额的释放为中段品牌和新入局品牌提供了更多的市场空间。

冠捷(AOC):虽整体受限于显卡供应紧张,但得益于其供应链优势,电竞呈现小幅增长。曲面电竞明显收缩,高分市场占比收缩;专业色彩显示器市场份额稳定,便携显示器成长迅速。2021年出货规模468万台,同比下滑10%,实际出货规模和规划目标有4%的差距;2022年规划出货450万台左右,规划较保守。2022年整体策略由追求规模增长转变追求利润增长。

飞利浦(Philips):2021年其尺寸结构受供应影响较大,在主要消费产品线中,23英寸以下的小尺寸产品供应紧张,尤其是21.5英寸出货量快速下降;入门级商用系列因成本问题缺乏价格竞争优势,二季度开始份额环比下滑,下半年缺乏增长动力。2021年出货规模270万台,同比下滑5%,实际出货规模和规划目标存在4%的差距;2022年规划出货250万台左右,收缩幅度较AOC更大。2022年飞利浦在市场布局上将与AOC呈现一定的差异化,前者将在商用市场进行更明确的产品线调整,同时降低线下消费市场出货重心。明年飞利浦对于线上市场的出货目标仍然相对积极。

联想(Lenovo):2021年联想在独立显示器市场取得了令人瞩目的增长,主要依托于其多品牌策略,ThinkVision侧重商用市场,Lecoo作为消费市场的急行军,增强了DIY市场的影响力,同时引入新品牌异能者进入显示器市场。2021年联想独立显示器出货规模约247万台,同比增幅达63%。得益于信创项目,2021年B2B增幅达到73%;B2C增幅为53%,增长主要得益于DIY市场,Lenovo和子品牌Lecoo在DIY市场都有良好表现。2022年规划出货285万台左右,明年B2B增幅会收缩,增长将主要来自于消费市场。

戴尔(Dell):2021年上半年备货不力,影响了出货表现,进而制约了其在主力专业色彩显示器市场的表现,27英寸等大产品占比收缩;为缓解通用机型的供应难题,Dell导入大陆新进面板厂商,三季度19.5及23.8英寸供应略有改善,随着下半年整体供应情况的改善,出货规模重回佳境。2021年出货规模156万台,同比增幅20%。2022年规划出货190万台左右,追求同比22%左右的增长。

三星(Samsung):2021年在疫情影响下,三星越南工厂生产困难,整体供应状况转差,同时23.8英寸产品价格仍保持高位,对需求形成明显抑制,但其在消费市场主力的27英寸产品价格策略相对积极;曲面电竞占比较高使得其电竞出货受到一定影响。2021年三星出货规模约151万台,同比增长20%。2022年规划出货180万台左右,明年整体策略体现为积极寻求产品结构升级。

电竞市场:增长陷入瓶颈期,供应为主要掣肘,240Hz崭露头角

中国电竞显示器市场2021年下半年出货未达到预期,低于预期的因素主要包括两个方面:一方面,由于自身本土疫情反复,使得许多网咖再次进入停业状态,网咖需求仍旧比较低迷;另一方面,因显卡供应没有得到明显改善,无论是线上还是网咖,电竞需求都受到抑制或转移。

群智咨询(Sigmaintell)数据显示,2021年中国电竞显示器出货规模约360万台,同比增长仅1%。参考历史同比增幅数据,可观察到今年是自中国电竞市场开局以来增速最低的一年。2022年,结合显卡供应时间节奏、品牌出货心态,以及本土疫情防控的严格化趋势,整体缺乏强劲增长的动力,因此2022年出货规模预计约为420万台,同比小幅增长16%。

虽然市场规模增量有限,但2021年中国电竞市场展现出了结构升级的积极变化,主要表现为240Hz崭露头角。2021年中国电竞市场240Hz出货量约18万台左右,在电竞市场的渗透率接近5%。在头部品牌冠捷以及华硕(ASUS)等专业电竞品牌的产品策略带动下,2022年240Hz出货规模预计在38万台左右,渗透率接近9%,迎来发展元年。

曲面市场:低谷期到来,供应链调整与成本上涨为主因

2021年中国曲面显示器市场出货规模约为240万台,同比下滑达36%。下滑原因主要在于曲面整体供应情况并未出现明显改观,终端价格仍处于较高水位。就目前对于终端均价的监测情况而言,除曲面市场外,各个细分市场均价均已开始回落,但曲面终端价格涨幅仍进一步扩大。加之电竞显卡对于电竞显示器的影响,曲面电竞占比进一步下滑,使得曲面市场规模呈现快速收缩。

总体可见目前曲面供应紧张和显卡紧张对曲面电竞的负面影响,造成曲面市场步入“低谷期”,在这两个负面因素缓解后,有望迎来曲面市场的反弹式增长。

宽屏市场:缓速增长,次年供应改善和多元化发展方向将释放新机会

2021年中国宽屏显示器市场进入下半年后,呈现出复苏态势,复苏的动能主要是来自于品牌格局的变化,市场增量是由新入局品牌华为所带动。

2021年宽屏出货规模超过55万台,同比增长7%左右。结合2022年宽屏面板将成倍级增长以及多元化发展的趋势,群智咨询(Sigmaintell)预计中国宽屏市场同比将获得19%左右的增长。

线上市场:增长受限,但重心优势凸显,次年有望保持

疫后线上工作、学习的生活新型态形成,显示器转为刚性需求,加速线上消费习惯的转变和养成,在中国独立显示器市场中线上市场占比逐季增加。2021年上半年中国独立显示器线上市场销量接近400台,下半年销量预计为410万台左右。

在线上市场中,冠捷占比在三成左右,线上渠道整体乏力,2021~2022年将持续负增长;飞利浦线上渠道受价格波动及自身重视程度影响,占比仅两成左右,但明年将加强线上渠道能力;戴尔和三星线上渠道占比均衡,保持在五成左右。

群智咨询(Sigmaintell)数据显示,2021年中国线上显示器市场销售规模约为820万台,同比微幅增长 1%。2022年,受品牌重心整体向线上倾斜以及渠道注重商用发展策略的影响,预计中国线上显示器市场将持续增长,有望突破850万台以上。

群智咨询(Sigmaintell)建议:后疫情时代下,市场风险和机会共同放大

进入了后疫情时代,展望2022年中国显示器市场,仍然会是风险和机会共同放大的一个关键时间节点。从风险面看,在宏观层面上,中国内需经济仍将继续承压;在中观层面上,显示器消费市场的主力人群失业率持续增长;在微观层面上,人们的消费支出转向保守。种种因素叠加,2022年中国显示器市场的需求风险被明显放大。

但从机会面看,市场发展仍然具有良机。第一,供应形势明显改善。伴随着全球电子消费品类疫情红利的逐步消退,显示器面板供应将显著改善;第二,成本形势转变,受供应改善的影响,显示器面板成本也迎来调节,面板价格将去水分化,有利于终端售价的企稳和回落;第三,显示器供应竞争激烈化,将有利于推动高端技术下沉和市场结构升级,尤其在240Hz、宽屏、MiniLed、OLED等高端技术方面。综上所述,群智咨询(Sigmaintell)提出以下两方面建议:

1. 布局合理完善的产品线。清晰明确的对产品线进行规划,针对目标客户和自身品牌特性,合理进行产品线梳理,实现全面覆盖目标客户,精准展现品牌定位。针对消费市场和商用市场的不同属性,对尺寸、分辨率、刷新率以及平曲结构上进行灵活且针对性的产品升级,增强市场竞争力。

2. 紧抓电竞显示器趋势。目前除电竞显示器外的细分市场规模发展较为缓慢,因此重点挖掘电竞显示器市场是重中之重。针对普通玩家和电竞玩家进行产品线区隔,前者重视屏幕综合性能,强调性价比;后者则更加细分化,针对玩家的游戏属性进行专业化产品线布局,强调专业性,针对高刷、超高刷以及高分进行选择性强化。

提交右侧信息,了解更多会员服务方案;

或直接联系我们:

+86 151-0168-2530