In 22Q2, the multi-point spread of the epidemic across the country and the closure-control measures disrupted the steady growth of the auto industry. Analyzing the national auto sales data in April, it fell 48% YoY, the most significant decline in recent years. Entering May, to quickly recover the industry losses caused by the early closure and control, the national level successively launched several measures such as sending cars to the countryside and extending subsidies and urged local governments to actively introduce local auto market stimulus policies, which is expected to promote the rapid development of the auto industry’s rebound. Overall, the auto market conditions improved in May, and consumers’ demands for car purchases were released to a certain extent. In June, the epidemic prevention and control situation gets further loose compared to May. The production and work resumption in Shanghai and surrounding areas continued to accelerate. The supply problem of automobiles’ components will be effectively alleviated. It is expected that the demand for car purchases suppressed by the epidemic in the early stage will be released in June, the domestic automobile market will gradually return to normal levels, and the monthly sales volume will also turn from negative to positive YoY. However, due to the excessive loss of automobile production and sales in the first half of 2022, Sigmaintell predicts that the domestic automobile sales in 2022 will be about 26.3 million units, which are expected to be the same as the sales in 2021 and is difficult to show significant growth.

Data source: China Automobile Association, Sigmaintell

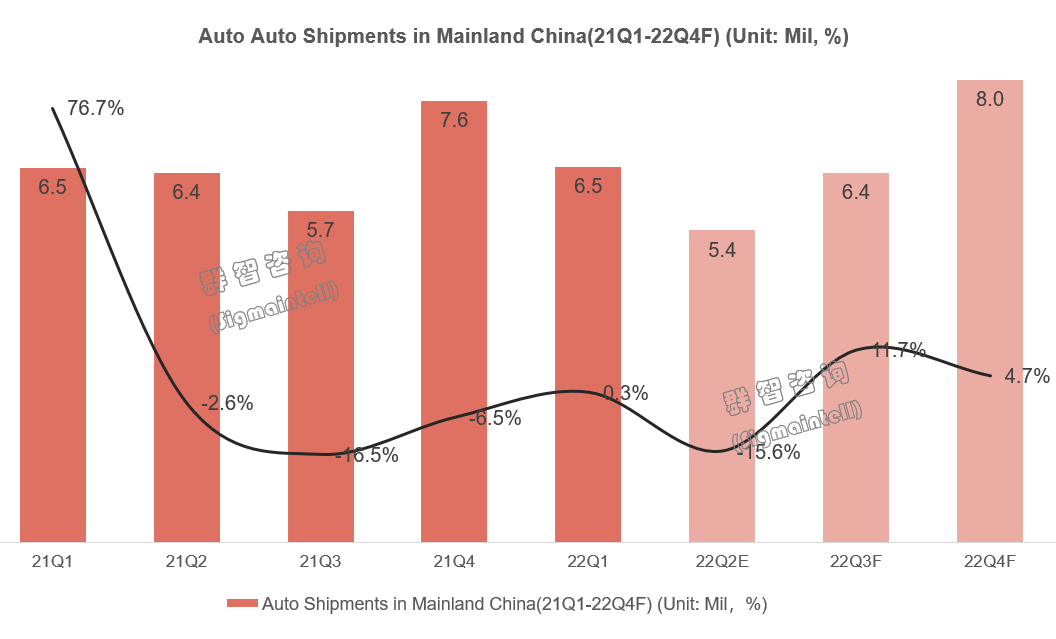

Auto Market: The domestic auto market sales in May were about 1.77 million, which decreased 17% YoY

According to data from the China Automobile Association, in May 2022, domestic car sales (including fuel and electric) were about 1.77 million, which decreased 17% YoY. However, the recovery trend was noticeable compared to April. From January to May, the cumulative domestic car sales were about 9.46 million units, a YoY decrease of 13%. Since the beginning of 2022, the automobile market's supply and demand sides have faced significant pressure.

Supply-side: The epidemic occurred in many places in the first quarter. The closure control policy and logistics restrictions caused some Auto factories and supporting supply chain factories to stop production. At the same time, the prices of automotive raw materials such as power batteries, chips, steel, and aluminum continued to rise, driving up manufacturing costs, and many car companies have announced price hikes.

Demand-side: Affected by the complex and severe international environment and the unexpected impact of the domestic epidemic, the downward pressure on the economy has further increased, and the weak demand from downstream consumers is particularly evident. To revitalize the auto market, relevant policies have been introduced at the national level to promote automobile consumption, followed by policies in various provinces and cities. By sending coupons, car purchase subsidies, lottery draws, etc., money has been used to increase automobile consumption. The subsidies include buying a new car, trade-in a motorcycle for an auto, trade-in an old one for a new one, etc. The sales of most car companies in May rose sharply MoM, and the auto market showed apparent signs that it is gradually improving.

Sigmaintell predicts that domestic auto sales in June are expected to reach 2.4 million units, a YoY increase of 20%. This will also be the first sign of a recovery in the auto industry in the past six months. As the policy to maintain the stability of the auto market continues to advance during the year, the growth trend is expected to continue in the year’s second half. According to the forecast of Sigmaintell, the car sales in the second half of 2022 will reach 14.4 million units, an increase of 8.3% YoY.

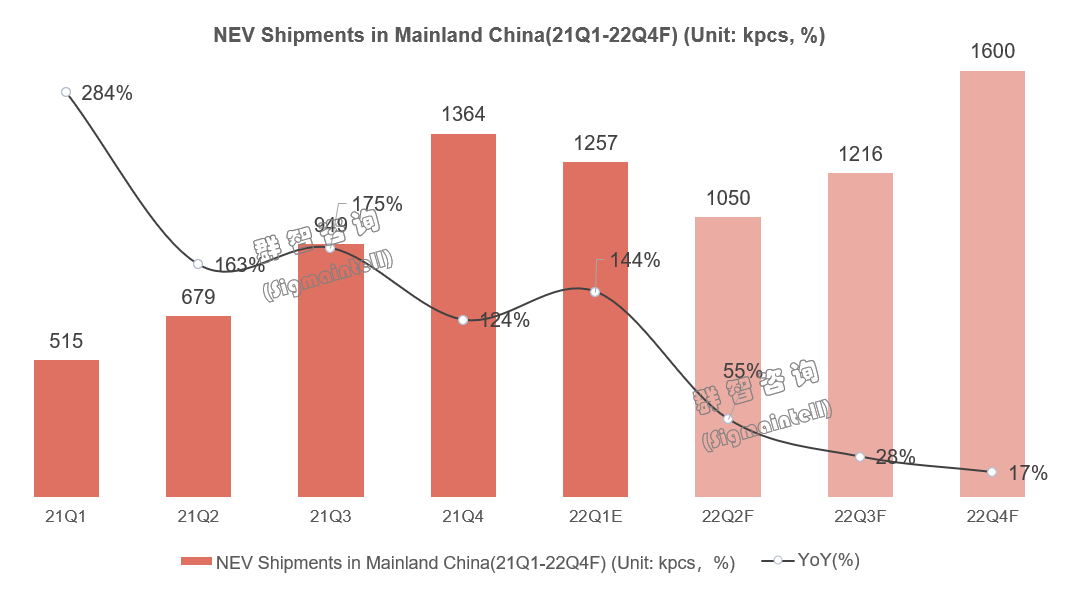

New energy: New energy car companies accelerate the recovery of the Auto market

With the continuous implementation of the resumption of work and production in various places, and the dual efforts of the demand side and the supply side, after the sales of new energy vehicles fell sharply in April, they sounded the clarion call for the recovery of the auto market as a leader in May. The production capacity is also gradually returning to the level before the lockdown, and the auto market is expected to regain its growth momentum. The new energy vehicles are the focus of this series of auto incentive policies. A new round of new energy vehicles going to the countryside policy is expected to accelerate the increase in the penetration rate of new energy vehicles in the sinking market. Sigmaintell predicts that domestic new energy vehicles’ sales are expected to exceed 5 million annually

Data source: official website of the automobile company, Sigmaintell

From the perspective of manufacturers, their specific performances are as follows:

BYD

BYD maintained a high growth rate in May, with sales of about 115,000 units and a YoY growth rate of 154%. BYD's new energy vehicles have maintained monthly sales of more than 100,000 units for three consecutive months. Its unique supply chain system makes obvious advantages in guaranteeing ordinary supply during the epidemic. Among them, the sales of Pure Electric Vehicles (BEV) were 53,000 units, a YoY increase of 185%, and the sales of Han/Yuan plus EV and other models performed well. Plug-in Hybrid Electric Vehicles (PHEV) sales were 61,000 units, a YoY increase of 369%. The sales of high-priced models such as Song Plus DM-I have increased, and the product structure has been continuously optimized. The recently released Denza D9 and Seal models have strong competitiveness and excellent performance and are equipped with a series of innovative technologies, which are expected to become popular models. From the perspective of medium and long terms, BYD will keep the competitiveness of new models launched in the future through the innovation and iteration of a series of industry-leading self-developed technologies such as E-platform 3.0, DMi, CTB, and iTAC and help the brand value continue to rise.

NIO

NIO has shaken off the haze of the shutdown in April. The sales in May were about 7,000 units, an increase in both MoM and YoY. Among them, 1707 units of ET7 equipped with the NT2.0 platform were delivered, a YoY growth of 146%. After the relevant supply chain enterprises resume work and production, it is expected that the production of new cars will be further resumed in June, and the delivery of models, including the ET7, will continue to accelerate. The SUV model ES7 equipped with the same NT2.0 intelligent driving platform will also be released soon, which indicates that NIO is about to usher in a period of significant market power. At the same time, the NIO smart cockpit hardware upgrade plan consisting of Snapdragon 8155 chip, smart gateway, high-definition camera, 5G module, and others will also be announced together, and NIO is expected to return to the top three sales of new power brands within this year. In addition, it is reported that NIO will launch a new sub-brand Gemini this year, which means “The Two main stars of the constellation Gemini.” This new sub-brand will further complement the existing high-end models to increase the market size.

Xiaopeng

Xiaopeng delivered 10,100 autos in May, a YoY increase of 78%, With an accumulative delivery of 537,000 units in the first five months, a YoY growth of 122%. With the acceleration of the resumption of work and production in the core supply chain, Xiaopeng has resumed two shifts of normal production at the Zhaoqing factory in mid-May to accelerate the delivery of a significant number of orders accumulated since the first quarter. Besides, in addition to the Xiaopeng G9, the first model to enter the mid-to-high-end market, Xiaopeng plans to build new models of the B-class and C-class auto platforms in 2023, which will enable the auto brand to cover the mid-range CN¥150,000 to the high-end CN¥400,000 fully. This new platform technology will be benchmarked with Tesla, which will further enhance the competitiveness of cost control, and is expected to improve the operating conditions of car companies structurally.

Li

Li Auto sold 11,500 units in May, a YoY increase of 166% and a MoM increase of 176%, leading the sales of new power brands in May by a slight advantage. Li delivered about 47,000 vehicles from January to May this year, a YoY increase of nearly 111%. Li’s sales continued to halve during the epidemic season, March and April. However, with the recovery of the supply chain, the production capacity gradually increased in May, and the sales gradually returned to normal. It is reported that the Ideal L9 will be officially released on June 21 and formally delivered in August. The launch of the new car will provide more choices for downstream consumers and is expected to raise the brand’s sales to a new level.

Leapmotor

Leap Motor has been less affected by the epidemic because of its multi-enterprise supply and multi-regional planning supply chain approach. Leap Motor once "led" the new force with sales of 9,087 units in April this year and maintained steady growth in May with sales reaching 10,000 units, a YoY growth rate of over 200% for 14 consecutive months. In May, Leapmotor officially pre-sold its model Leapmotor C01. Both Leapmotor C01 and Leapmotor T03 participated in a new round of new energy vehicles going to the countryside. Compared with the relatively high prices of new power models such as NIO’s “Wei Xiaoli,” the average selling price of Leap Motor vehicles is relatively low. So Leap Motor will be one of the primary beneficiaries of this round of going to the countryside policy and is expected to maintain a rapid YoY growth trend in the second half of the year.

Neta

Neta Auto achieved sales of 11,000 units in May, a YoY increase of 144%, and an MoM increase of 25%. Achieved a continued YoY growth for 23 consecutive months since July 2020 and delivered nearly 50,000 units in the first five months of 2022, a YoY increase of 213%. Neta has firmly stood in the first camp of the new car-making forces. The unexpected superposition of the ups and downs of the epidemic and supply chain shortages still severely impact new energy vehicles. Under this background, Neta Auto has actively made efforts in product services and other aspects to expand its product matrix and realized many achievements, laying a solid foundation for the brand’s long-term development. Its recently released Tiangong battery solves several major pain points in driving safety, battery life, and battery lifespan. It is expected to achieve epoch-making performance and continue to release positive brand development momentum.

AITO

AITO Auto is a luxury electric vehicle brand launched by AITO. At present, only one model, Wenjie M5, has been launched. Its sales volume in May was 5,006 units, achieving an MoM increase of 54%. For a model under a brand-new brand, its cumulative sales exceeded 10,000 in just three months and set the fastest record for a single model of the new brand, and the performance is excellent. In addition, AITO will launch a large electric SUV, Wenjie M7, and its estimated delivery time will start in July. Benefiting from the rising period of the new energy vehicle market and the empowerment of the Huawei brand HarmonyOS smart cockpit, AITO is expected to use intelligence as a breakthrough point in the field of extended-range electric vehicles and promote the reform of the entire automobile industry. Its goal of achieving over 10,000 sales of a single model this year is also close at hand.

Outlook

According to the forecast of Sigmaintell, with a series of new energy vehicle reduction policies issued at the national level are superimposed with local subsidies, the domestic sales of new energy vehicles in 2022 are expected to exceed 5 million units, a YoY increase of 46%, and the penetration rate will reach nearly 20%. From a quarterly perspective, in the second quarter, the epidemic caused the production to shut down and thus making the sales volume decline MoM. With the continued progress of resumption of production and the blessing of consumer policy subsidies, it is expected that the new energy vehicle market will be significantly better than the same period last year starting from the third quarter. The fourth quarter is expected to reach a single quarter sale of 1.6 million units.

Data source: China Automobile Association, Sigmaintell

Overall, the proportion of new energy vehicles in the overall automobile market continues to increase. However, as traditional brands continue to increase investment in new energy, the market competition pattern will continue to deteriorate. For new power brands, national supporting policies such as Auto Going to the Countryside are only a short-term benefit. As for the long-term development, more resource investments and product value outputs are needed to stabilize the brand’s competitive position, for which they have devoted a lot to build.

中文:

疫情后补贴政策频出,加速汽车市场回暖

2022年二季度,全国各地疫情的多点蔓延及封控措施打乱了汽车产业稳步增长的节奏,从4月份全国汽车销量数据来看,同比下滑48%,为近年最大下降幅度。进入5月份,为了更加迅速地挽回因前期封控造成的行业损失,国家层面陆续推出了汽车下乡、补贴延期等多项举措,并敦促各地积极出台地方性车市刺激政策,有望推动汽车产业快速反弹。总体看来,5月汽车市场状况有所改善,消费者购车需求得到一定释放,而进入6月疫情防控形势相比5月进一步放宽,上海及周边地区复工复产持续加速,汽车及零部件的供应问题将得到有效缓解,预计前期受疫情抑制的购车需求,在6月份将集中释放,国内汽车市场将逐渐恢复到正常水平,月销量同比也将由负转正。但由于2022年上半年汽车产销损失过多,群智咨询(Sigmaintell)预测,2022年全年国内汽车销量约为2630万辆,预计与2021年销量基本持平,难以呈现显著增长。

车市篇:5月份国内汽车市场销量约177万,同比下降17%

根据中汽协数据,2022年5月份国内汽车销量(含燃油+电动)约177万,同比下滑17%,但相比4月回暖趋势明显。纵观1~5月,国内汽车累计销量约为946万台,同比去年下降13%,2022年开年以来汽车市场供需两端都面临较大压力。

供应端:一季度疫情多地出现,封控政策、物流受限导致部分整车及配套供应链工厂停产,同时动力电池、芯片、钢材、铝材等汽车原材料价格持续上涨拉高制造成本,多家车企纷纷宣布涨价。

需求端:受复杂严峻的国际环境和国内疫情冲击的超预期因素影响,经济下行压力进一步增加,下游消费者需求疲软的情况尤为明显。为振兴车市,国家层面出台了相关政策促进汽车消费,随后全国各省市政策也陆续出台,通过发放消费券、购车补贴、抽奖等方式,用真金白银加大汽车消费的力度,其中补贴包括直接购买新车、以摩换汽、以旧换新等形式。多数车企5月份销量实现环比大涨,汽车市场释放出正逐渐回暖的良好迹象。

群智咨询(Sigmaintell)预测,国内汽车6月份销量有望达到240万辆,同比增长20%,这也将是近半年来首次看到汽车行业复苏的信号。随着维稳车市的政策在年内持续推进,预计下半年将继续保持增长趋势,根据群智咨询(Sigmaintell)预测,2022年下半年汽车销量将达到1440万辆,同比增长8.3%。

新能源篇:新能源车企吹响车市加速复苏号角

随着各地复工复产持续落地,需求端和供给端的双重发力,新能源汽车历经4月份的销量大幅下滑后,在5月以领航者的身份重新吹响了车市复苏的号角,产能也逐渐恢复至封控前的水平,汽车市场有望重拾高歌猛进的增长势头。而新能源汽车将是这一系列汽车鼓励政策的重点,新一轮的新能源汽车下乡有望加速推动下沉市场的新能源车渗透率提升,群智咨询(Sigmaintell)预测,全年国内新能源汽车车销量将有望突破500万辆。

各厂商来看,具体表现如下:

比亚迪(BYD)

比亚迪5月份继续保持增量高位,销量约11.5万台,同比增速达到154%,目前比亚迪新能源汽车已经连续3个月保持单月10万台以上的销量,其独特的供应链体系使其在疫情常态下保供的优势明显。其中,纯电车(BEV)方面销量为5.3 万台,同比增长185%,汉、元plus EV等车型销量表现优秀;插混车(PHEV)方面销量6.1万台,同比增长369%,宋Plus DM-i 等高价位车型销量占比提升,产品结构持续性优化。其近期发布腾势D9 和海豹两款车型竞争力较强,性能优异并且搭载了多项创新型技术,有望形成爆款。从中长期来看比亚迪将通过e平台3.0、DMi、CTB、iTAC 等一系列行业领先自研技术的推陈出新及迭代,使得后续推出的新车型保持竞争力,助力汽车品牌价值持续向上。

蔚来汽车(NIO)

蔚来汽车挥去4月停工停产的阴霾,5月份销量约7千台,同比环比实现双增,其中搭载NT2.0平台的ET7交付1707台,同比增长146%。相关供应链企业复工复产后,预计6月份新车生产还将进一步恢复,包括ET7在内的车型交付将继续提速,搭载同款NT2.0智能驾驶平台的SUV车型ES7也即将于发布,这预示着蔚来汽车即将迎来市场发力期。同时,由骁龙8155芯片、智能网关、高清摄像头、5G模块等组成的蔚来智能座舱硬件升级计划也将一并宣布,蔚来汽车有望于年内重回新势力品牌销量前三甲。此外,据悉蔚来在今年推出全新子品牌Gemini,意为"双子星",该品牌与现有高端车型进行互补从而进一步提高市场规模。

小鹏汽车(Xiaopeng)

小鹏汽车5月交付1.01万台,同比增长78%,前五月累计交付53.7万台,同比增长122%。随着核心供应链复工复产进度加快,小鹏汽车已于5月中旬恢复肇庆工厂的两班正常生产,以加速交付一季度以来累积的大量订单。另外,小鹏汽车除进军中高端市场的先行车型小鹏G9外,在2023年计划打造的B级车平台和C级车平台新车型,将使得汽车品牌全面覆盖中端15万元至高端40万元的售价区间,且该全新平台技术将与Tesla对标,使得成本控制上的竞争力进一步提升,有望从结构性上改善车企的经营状况。

理想汽车(Li)

理想汽车5月销量1.15万辆,同比增长166%,环比增长176%,以微弱优势领跑5月新势力品牌销冠。其今年1-5月累计交付约4.7万辆,同比增长约111%。在受国内疫情肆虐的3、4月份销量一度腰斩,但随着供应链恢复,5月份产能逐渐爬升,销量也日趋回归正常。据悉理想L9将于6月21日正式发布,8月开始正式交付,新车上市将给下游消费者提供更多选择,并有望使品牌销量再次上升一个台阶。

零跑汽车(Leapmotor)

零跑汽车因其供应链采取多企业供应及多区域规划的方式,受疫情冲击较小,曾在今年4月以9087辆的销量“领跑”新势力销冠,而5月份继续保持着稳健增长,销量达到1万台,同比增速连续14个月超过200%。5月份,零跑汽车正式预售了旗下车型零跑C01,该车型与零跑T03均参与了新一轮新能源汽车下乡活动。相对于蔚小理等新势力车型较高位的售价,零跑汽车平均售价相对较低,其将会是此轮下乡政策的主要受益车企之一,下半年有望继续保持同比高速增长的趋势。

哪吒汽车(Neta)

哪吒汽车5月实现1.1万台销量,同比增长144%,环比增长25%,实现自2020年7月以来连续23个月同比增长,2022年前五月累计交付近5万台,同比增长213%,已稳居造车新势力第一阵营。跌宕起伏的疫情及供应链短缺等超预期叠加对新能源汽车影响依旧严峻,此背景下哪吒汽车主动在产品服务等方面发力,扩容产品矩阵并取得多项成果,为该品牌长远发展奠定了扎实有力的基础。其近期发布的天工电池,解决了行车安全、电池续航与寿命几大痛点,有望实现划时代的性能表现,持续释放积极向上的品牌发展动力。

金康赛力斯(AITO)

AITO汽车是金康赛力斯推出的豪华电动车品牌,目前仅推出问界M5一款车型,其5月销量5006辆,实现环比54%增长。对于一款全新品牌旗下车型,仅在短短三个月累积销量破万并创下新品牌单款车型最快纪录,表现十分优异,此外年内AITO还会推出一款大型电动SUV问界M7,预计将在7月开启交付。受益于新能源汽车市场的上升期,以及华为品牌HarmonyOS智能座舱的赋能加持,AITO有望在增程式电动车领域以智能化为突破口,推动整个汽车行业的变革,其年内实现单一车型销量过万的目标也已近在咫尺。

展望篇

根据群智咨询(Sigmaintell)预测,国家层面出台的一系列新能源汽车下降政策叠加各地方补贴,国内新能源汽车2022年销量预计将有望突破500万辆,同比增长46%,渗透率将达到近20%。分季度来看,二季度中因疫情导致的停工停产问题销量环比下滑,随着复工复产持续推进,以及促进消费政策补贴的加持,预计三季度开始新能源汽车市场将明显好于去年同期,四季度有望达到单季160万台销量。

总体来看新能源汽车在整体汽车市场占比在持续提升中,但随着传统品牌不断加大新能源方向的投入,市场竞争格局也将不断恶化。对于新势力品牌来说,汽车下乡等国家政策的扶持只是短暂的利好,纵观长远发展则还需要更多的资源投入及产品价值输出,才可以稳固其倾心倾力打造的品牌竞争地位。